Total a annoncé mardi qu’il avait commencé à exploiter à Pau son supercalculateur Pangea III, le plus puissant ordinateur du monde dans l’industrie avec une puissance de calcul de 25 petaflops (millions de milliards d’opérations par seconde).

Pangea III est onzième au classement toute catégories des ordinateurs, derrière des machines installées dans de grands centres de recherche aux États-Unis, en Chine, au Japon ou en Europe. Le groupe pétrolier a investi “plusieurs dizaines de millions de dollars” dans ce troisième supercalculateur, a confirmé une source proche du dossier à l’AFP.

La machine porte la puissance de calcul totale du groupe à 31,7 petaflops (soit 170 000 ordinateurs portables). Elle triple sa capacité de stockage à 76 petaoctets (près de 50 millions de films en HD).

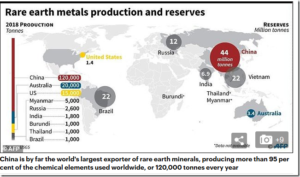

The recent threats by Beijing to cut off American access to critical mineral imports has many Americans wondering why our politicians have allowed the United States to become so overly-dependent on China for these valued resources in the first place.

Today, the United States is 90 percent dependent on China and Russia for many vital “rare earth minerals.”

The main reason for our over-reliance on nations like China for these minerals is not that we are running out of these resources here at home. The U.S. Mining Association estimates that we have at least $5 trillion of recoverable mineral resources.

The U.S. Geological Survey reports that we still have up to 86 percent or more of key mineral resources like copper and zinc remaining in the ground, waiting to be mined.

These resources aren’t on environmentally sensitive lands, like national parks, but on the millions of acres of federal, state and private lands.

The mining isn’t happening because of extremely prohibitive environmental rules and a permitting process that can take 5-10 years to open a new mine. Green groups simply resist almost all new drilling.

What they may not realize is that the de facto mining prohibitions jeopardize the “Green Energy Revolution” that liberals so desperately are seeking.

How is this for rich irony: To make renewable energy at all technologically plausible, will require massive increases in the supply of rare earth and critical minerals.

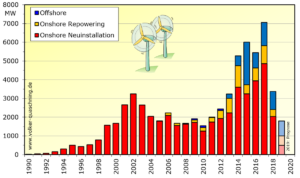

Despite all the talk about the need to transition over to green energies, Germany’s progress — in especially wind energy — has ground to a complete halt.

German news site iwr.de here reports that the expansion of wind energy in Germany has “come the a stop” as the government has scaled back subsidies and enacted stricter permitting laws.

“As in April 2019, only nine new wind turbines went into operation nationwide in May,” IWR reported. “The year 2019 threatens to be a disaster for the wind industry in Germany.”

The IWR reported further: “In the first five months of 2019, only around 60 new onshore wind turbines went into operation nationwide. This is the result of an IWR evaluation of data from the market master data register of the Federal Network Agency (BNetzA).”

“A catastrophe” for wind power

At Twitter green energy activist Prof. Volker Quaschning called the collapse a “catastrophe”, tweeting that the expansion of wind power “collapsed completely”. He added that “it will be impossible to meet the CO2 reduction targets” and that 40,000 jobs in the wind industry are “on the brink”.

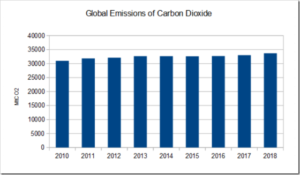

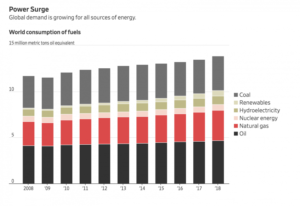

Global primary energy consumption grew rapidly in 2018, led by natural gas and renewables. Nevertheless, carbon emissions rose at their highest rate for seven years

Energy developments

Primary energy consumption grew at a rate of 2.9% last year, almost double its 10-year average of 1.5% per year, and the fastest since 2010.

By fuel, energy consumption growth was driven by natural gas, which contributed more than 40% of the increase. All fuels grew faster than their 10-year averages, apart from renewables, although renewables still accounted for the second largest increment to energy growth.

China, the US and India together accounted for more than two thirds of the global increase in energy demand, with US consumption expanding at its fastest rate for 30 years.

Carbon emissions

Carbon emissions grew by 2.0%, the fastest growth for seven years.

by Graham Hill, June 13, 2019 in GWPF/TheAustralian

Global coal production (up 4.3 per cent) and consumption (up 1.4 per cent) has increased at their fastest rate for five years.

Average global greenhouse gas emissions are rising at double the rate of Australia’s, exposing the mismatch between the “hope and reality” of meeting Paris Agreement goals, a report has found.

A major report by energy giant BP said the world was returning to coal, and without shale gas from the US and LNG exports from Australia the emissions reduction picture would be much worse.

Massive investments in renewable energy were needed but would not be enough to satisfy increasing demands for power, most notably in China and India.

BP said global emissions overall were up 2 per cent last year as the unexpected return to coal gathered pace.

World-wide energy demand grew at its fastest rate since 2010

The shale revolution powered U.S. oil and gas production in 2018 to the largest annual increases ever recorded by any country, according to energy giant BP PLC .

Surging global energy demand is fueling the production boom, even as oil and gas prices rise and economic growth slows, said BP’s annual statistical review published Tuesday.

World-wide demand for energy grew 2.9% in 2018, its fastest rate since 2010.

Unusual weather spurred some of the stronger-than-expected growth, as a greater number of extremely hot and cold days drove up air conditioning and heating use around the world, particularly in China, the U.S. and Russia, the company said.

In the U.S., energy consumption rose by 3.5% in 2018, with oil at 20.5 million barrels a day and a total of 817 billion cubic meters of gas consumed during the year.

German engineering, as good as it is, has not been able to eliminate the effect of “green” politics, which would replace fossil and nuclear power with renewables. The result is 172,000 localized blackouts in Germany in 2017.

Poverty was a constant companion of humanity until modern times. The proportion of people worldwide living in poverty was cut in half between 1990 and 2010, according to the World Bank, an achievement unprecedented in human history.

It was the result of a rapid boost in global energy production — up 43 percent during that period, according to the U.S. Energy Information Administration. Nearly 81 percent of that power was generated by fossil fuels, such as oil and gas.

A billion people around the globe still suffer extreme energy poverty, with no access to electricity. Everyone gets a hint of what that means when storms knock out the power, and everything in the house stops.

Fumbling occasionally for candles is a mere inconvenience, but life beyond carbon — entirely dependent on sunshine and a breeze — would be insanity.

In a letter to the UK’s Committee on Climate Change (CCC) on Wednesday (5 June), a team of scientists suggests that the CCC’s proposed target of net-zero emissions by 2050 will need almost all cars and vans on British roads to be electric-battery powered.

The team, which supports that goal, outlined the raw material needs and challenges that will come hand-in-hand with such an ambitious target. Current battery production requires materials like cobalt, copper and nickel.

Professor Richard Herrington of the Natural History Museum said in a statement that “there are huge implications for our natural resources not only to produce green technologies like electric cars but keep them charged”.

He and his colleagues calculated that switching all of the UK’s light vehicles to electric will require 207,900 tonnes of cobalt, 264,600 tonnes of lithium carbonate and over 2,300,000 tonnes of copper.

The reigning narrative of impending global environmental catastrophe dominates the airwaves and print media. Short of a drastic reduction in the use of fossil fuels, it is asserted, we are fast approaching the “end of days”. The demonization of fossils fuels in general, and coal in particular, has been wrought under pressure from special interests groups and organized lobbies of the climate-industrial complex where aspects of economic reality are caricatured or presented out of context. Complex trade-offs in energy policy are spun into tales of spurious simplicity, leading to misleading conclusions. Nowhere is this more apparent than in the debate over the role of coal-fueled power generation in Asia.

Opposition to the building of coal power plants in the poorer countries has been justified by environmental activists, banks and multilateral development agencies such as the World Bank in two key ways. The first revolves around the claim that climate change mitigation programs carry “co-benefits” for public health in developing countries. The second utilizes the assertion that renewable energy such as solar and wind power are effective substitutes for centralized grid electricity generated by fossil fuels.

The EIA AEO 2019 report shows that in year 2018 wind and solar energy resources provide about 3% of U.S. total energy consumption while fossil fuel energy resources provide about 81% of total energy use.

The dominate use of fossil fuels in meeting U.S. energy needs remains little changed from a decade ago before use of renewable energy resources became mandated and supported by lucrative government subsidizes.

Using additional EIA data the total wind and solar provided energy going back to year 2000 is available which allows an assessment of the Production Tax Credit (PTC) payments to be made.

In its Special Report n° 15 “Global warming of 1.5°C” (SR15) [1], IPCC proposes four scenarios to limit Earth temperature increase to 1.5°C. In all scenarios CO2 emissions are kept at virtually zero by 2050. These scenarios are based on the technology called Carbon Dioxide Removal (CDR) that will remove CO2 to compensate CO2 anthropic emissions.

“All pathways that limit global warming to 1.5°C with limited or no overshoot project the use of carbon dioxide removal (CDR) on the order of 100–1000 Gt CO2 over the 21st century. CDR would be used to compensate for residual emissions and, in most cases, achieve net negative emissions to return global warming to 1.5°C following a peak (high confidence). CDR deployment of several hundreds of Gt CO2 is subject to multiple feasibility and sustainability constraints (high confidence). Significant near-term emissions reductions and measures to lower energy and land demand can limit CDR deployment to a few hundred Gt CO2 without reliance on bioenergy with carbon capture and storage (BECCS) (high confidence)” (page 19).

IPCC defines “Carbon dioxide removal (CDR)” as follows : Anthropogenic activities removing CO2 from the atmosphere and durably storing it in geological, terrestrial, or ocean reservoirs, or in products. It includes existing and potential anthropogenic enhancement of biological or geochemical sinks and direct air capture and storage but excludes natural CO2 uptake not directly caused by human activities” (page 26).

The fourth scenario recognizes the logical and inevitable increase of CO2 emissions if the world continues its growth to remove poverty and allow Asia and Africa countries to develop. Therefore, this scenario is based on a massive use of the CDR techniques as the report says: “Emissions reductions are mainly achieved through technological means, making strong use of CDR“.

Indeed, CDR is just rebranding of the CCS concept that is a cul-de-sac technology for a lack of economy, a lack of available adapted geological sinks on the production sites and also a lack of population acceptance.

Les cours du baril d’or noir ont enregistré, en mai, leur première baisse mensuelle de l’année 2019, avec un repli de 11,4% pour le baril de Brent européen et de 15,8% pour son homologue américain, le “light sweet crude” texan ou “WTI“. Ce recul s’est accentué depuis mercredi dernier, porté par la frénésie taxatoire de Donald Trump à l’encontre de la Chine et désormais également du Mexique, qui fait peser des craintes sur la demande mondiale et détourne les investisseurs des valeurs dépendantes de cette croissance mondiale, dont l’or noir fait partie.

by P. Homewood, May 29, 2019 in NotaLotofPeopleKnowThat

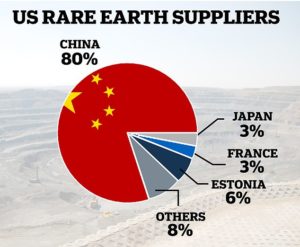

China has hinted that a trade war with the U.S. could lead to real war with a coded warning as it threatens to stop exporting essential ‘rare earth’ minerals.

A commentary in People’s Daily, the mouthpiece of China‘s ruling Communist Party, today said ‘Don’t say we didn’t warn you!’ – which is a diplomatic term usually reserved by Beijing to signal the start of an armed warfare.

China yesterday said it is ‘seriously considering’ restricting exports to the United States of rare earths, 17 chemical elements used in hospital scanners, nuclear power stations and LED lights.

China accounted for 80 per cent of rare earth imports between 2014 and 2017 to the United States.

by Eva Gomez, 28 mai 2018 in EnvironnementMagazine

Ce mardi 28 mai, le bureau d’études Enerdata publie son bilan énergétique mondial pour l’année 2018. Celui-ci fait part d’une hausse et de nouveaux records de consommation d’énergie et d’émissions de CO2.

En 2018, les pays du G20 ont vu leur consommation d’énergie augmenter de 2,1% et leurs émissions de CO21 de 1,7%, conclut Enerdata ce mardi 28 mai. Dans son nouveau bilan énergétique mondial, le bureau d’étude souligne que la croissance économique reste stable (+3,8%) dans les pays du G20, qui affichent néanmoins un niveau record de consommation énergétique. Dans l’Union européenne, les consommations d’énergie ont un peu diminué, mais cette baisse est compensée par une hausse de celles des Etats-Unis et des pays non membres de l’OCDE. « La consommation énergétique des USA a fortement augmenté, ce qui peut s’expliquer par les conditions climatiques extrêmes auxquelles ils ont été soumis, dont l’hiver très froid qui a demandé beaucoup de chauffage », explique le président d’Enerdata, Pascal Charriau. Par ailleurs, il semblerait que « le développement économique se fasse de façon énergivore : même si on observe un léger gain d’intensité énergétique, l’efficacité énergétique n’est pas améliorée », souligne-t-il.

by P. Homewood, May 26, 2019 in NotaLotofPeopleKnowThat

Taxpayers’ money earmarked to support overseas development has been spent on supporting China’s fracking industry, The Independent can reveal.

The government is required to spend 0.7 per cent of its national income each year on foreign aid.

But even with climate change threatening the developing world with droughts, flooding and heatwaves, millions have been spent on fossil fuel investment abroad over the past two years.

This includes two schemes aiming to “export the UK’s expertise in shale gas regulation” to China, as controversy about new drilling sites rages back in Britain.

I won’t bore you with the rest of the story. As you can probably guess, the “Independent” being the “Independent” proceeds to give full coverage to a load of eco cranks, including Christian Aid, who claim that the rapidly changing climate is driving more extreme weather, more acute disasters. (Don’t they know it’s a sin to lie?)

At the end they deign to give a few words to the government spokesperson.

Leaving aside the question why China needs our aid at all, the “Independent” fails to ask the really relevant question of why our government is so keen for us to decarbonise at huge cost, but at the same time thinks it is a good idea to help China develop their natural gas sector?

New Delhi: Fitch Solutions Tuesday said India’s thermal coal output is projected to grow at an average annual rate of 4.3 per cent by 2028. “In absolute volume terms, China and India will have the largest impact on the global coal market balance,” Fitch Solutions Macro Research said in a report.

It further said the surge in Chinese imports that occurred over 2015-2017 as a result of dramatic domestic production curbs was a temporary phenomenon.

“We forecast thermal coal production in China to stagnate at 0.5 per cent growth per annum from 2019 onwards, but not decline, as new coal mines in Inner Mongolia, Shaanxi and Shanxi provinces offset mine closures in the rest of the country,” it said.

Climate change was supposed to have won the party the Australian election. But yesterday, routed in the polls, panicking Labor Party leaders backed the opening of a coal field bigger than the UK to mining.

Fearing a wipeout in state elections next year amid a rising tide of pro-coal workers and a rebellion against its plans to halve Australia’s carbon emissions, the Labor state government in Queensland accelerated its decision on 105,000 square miles of coal-rich outback land known as the Galilee Basin.

It came days after the party lost what was dubbed as the “climate election” to the incumbent centre-right, pro-coal government of Scott Morrison, suffering the most damage with swings of up to 20 per cent in the coal country of central Queensland and the Hunter Valley of New South Wales.

Queensland’s premier, Annastacia Palaszczuk, announced she was overturning all attempts to block mining and all outstanding approvals would be resolved within three weeks. She said she was “fed up” with her own government’s processes, and that the election had been a “wake-up call” on mining the basin. The move was welcomed by the federal resources minister, Matt Canavan, who told The Times yesterday that the Galilee Basin represented a victory for the “hi-vis workers’ revolution” — a reference to the armies of mine workers, dressed in high-visibility shirts, who make Australia the world’s biggest coal exporter, and seemingly a reference to the “yellow vest” movement in France which battled President Macron on his climate policies.

Production from world uranium mines now supplies 90% of the requirements of power utilities.

Primary production from mines is supplemented by secondary supplies, formerly most from ex-military material but now the products of recycling and stockpiles built up in times of reduced demand.

World mine production has expanded significantly since about 2005.

All mineral commodity markets tend to be cyclical, i.e. prices rise and fall substantially over the years, but with these fluctuations superimposed on long-term trend decline in real prices, as technological progress reduces production cost at mines. In the uranium market, however, high prices in the late 1970s gave way to depressed prices in the whole of the period of the 1980s and 1990s, with spot prices below the cost of production for all but the lowest cost mines. Spot prices recovered from 2003 to 2009, but have been weak since then.

The quoted spot prices through to about 2007 applied only to day-to-day marginal trading and represented a small portion of supply, though since 2008 the proportion has approximately doubled, to about one-quarter in the last decade. Most trade is via 3-15 year term contracts with producers selling directly to utilities at a significantly higher price than the spot market, reflecting the security of supply.* The specified price in these contracts is, however, often related to the spot price at the time of delivery. However, as production has risen much faster than demand, fewer long-term contracts are being written.

In the context of the European elections, European Scientist is bringing you an series of views from experts from different countries on various topics around science and science policy in Europe, to provide an overview and analysis, which will be useful for the next commission.

ES: What is your assessment of energy policy in Europe? What have the major achievements of the outgoing commission been?

The greatest success of the outgoing commission is to have developed a policy to support gas interconnections by financing projects of common interest. The aim is that every single methane molecule that enters the territory of the Union can circulate to any other location. This will help to diversify gas supply sources, particularly from the south of the Union (thanks to more gas arriving as LNG and via the Southern Corridor).

ES: There is a wide disparity in energy policy between different countries (e.g. France and Germany). Do you think it is necessary to harmonise policy or on the contrary is it preferable to maintain diversity?

La Commission européenne a publié dès le début de l’année 2019 son rapport sur l’évolution des prix et coûts de l’énergie en Europe. On peut y lire que l’étude de ces coûts devrait conduire à « veiller à̀ ce que les entreprises ne soient pas désavantagées ni écartées » et que « les prix de détail (réels) dans l’Union sont plus élevés qu’aux États-Unis, au Canada, en Russie, en Chine et en Turquie, mais inférieurs à̀ ceux observés au Japon et au Brésil. » Le graphique suivant (Figure 1) illustre bien le fait que les industries européennes sont pénalisées par rapport aux entreprises d’autres pays qui sont des concurrents directs sur les marchés internationaux, y compris pour nos importations. Le rapport ajoute pudiquement, sans y insister que « l’évolution des prix de l’électricité est dominée par les taxes et prélèvements ».

In the Joint EU-US Statement of July 2018 agreed by President Jean-Claude Juncker and U.S. President Donald Trump, it was decided to strengthen strategic transatlantic cooperation on energy. In particular, the European Union expressed its ambition to import more liquefied natural gas (LNG) from the United States to diversify its energy supply.

In the end of April U.S. liquefied natural gas exports to the EU were up by 272%. It is in this context that on Tuesday 14 May, Vice-President Maroš Šefčovič in charge of the Energy Union will join the President of the United States Donald Trump in getting a first-hand look at the Cameron LNG export terminal in Hackberry in the U.S. State of Louisiana, which is expected to launch first shipment in the second half of this year.

As the pressure mounts in Germany to switch off coal power plants and to rapidly transition over to green energies, one gets the feeling that it all has more to do with a desperate, last-ditch effort by the green energy proponents to rescue their pet green project.

Behind closed doors, no one in Berlin believes in it

Now, just days ago, energy expert Dr. Björn Peters wrote at the German Association of Employers site that the Energiewende has deteriorated to the point that: “No specialist politician in Berlin believes in the success of the Energiewende any more. Whoever you ask, everyone says this only behind closed doors and thinks that if you go to the press with it you can only lose against the ‘green’ media mainstream.”

Peters warns that what is needed in Germany is a good dose of reality and “a fresh start on energy policy.”

Advantages of fossil fuels “too great”

The German expert writes that despite the hundreds of billions of euros committed to green energies, “chemical energy from coal, oil and gas supplies about four fifths of primary energy worldwide and also in Germany and thus represents the present energy supply”.

SYDNEY – In a corner of the Australian Outback, a drilling crew will soon try tapping shale rocks that could hold more than three times the world’s annual consumption of natural gas.

Origin Energy Ltd. plans to drill two wells later this year in the Northern Territory’s Beetaloo Basin, after the local government ended a three-year ban on fracking — the practice of extracting oil and gas from layers of shale rock deep underground. With an estimated 500 trillion cubic feet (14 trillion cubic meters) of gas, Beetaloo has been compared to famed U.S. shale regions such as Marcellus and Barnett.

But its isolated location, lack of infrastructure and the likelihood of tough environmental opposition make Beetaloo a highly speculative investment.

“There are some big numbers being quoted, and people have to realize this is exploration,” said Mark Schubert, Origin’s head of integrated gas, noting that only some of the total reserves would be extractable.

Dans un contexte de remise en question des voitures à moteur thermique et de lobbying pour en interdire la vente, à brève échéance, on serait bien avisé avant de se précipiter dans un tel changement radical et brutal de paradigme, de s’interroger sur la pertinence de son urgence et, partant, sur une approche plus pragmatique tenant compte des réalités socio-économiques.

ll faut d’abord rappeler que la marché de la voiture est mondial et qu’il est de plus en plus conditionné par les politiques des pays émergents et en développement qui ont comme souci prioritaire d’assurer leur croissance économique et d’améliorer les conditions de vie et le confort de leur population. La voiture en fait partie ! Ces mêmes pays sont également fort préoccupés, à juste titre, par la pollution de leurs villes [1]. Or celle-ci provient nettement plus de la production de chaleur dans les secteurs industriels, des services et du logement, que de la circulation automobile.Ce n’est donc pas cette dernière qui, pour ces pays, est la cible prioritaire pour assainir l’air urbain, mais plutôt le mode et l’efficacité de génération de calories dans les secteurs précités. D’ailleurs, le marché des voitures à moteur thermique, connaît une croissance soutenue dans le monde ces dernières années (en moyenne 3%/an). Sur les 98 millions de voitures neuves vendues en 2018, il n’y aurait qu’à peine plus d’un million de véhicules électriques (VE) [2] et très peu de véhicules à hydrogène. Alors que tous les fabricants investissent dans le développement des VE, la très grande majorité d’entre eux dont tous les européens et même Toyota qui y avait consacré des recherches approfondies, ont abandonné l’option hydrogène.

…

La géologie, une science plus que passionnante … et diverse